Market Recap: earnings, earnings, earnings

Markets advanced in May, supported by strong corporate earnings and continued enthusiasm for technology, including artificial intelligence (AI). At the same time, geopolitical risks resurfaced, reminding investors that volatility remains a feature, not just a “bug,” of the current environment.

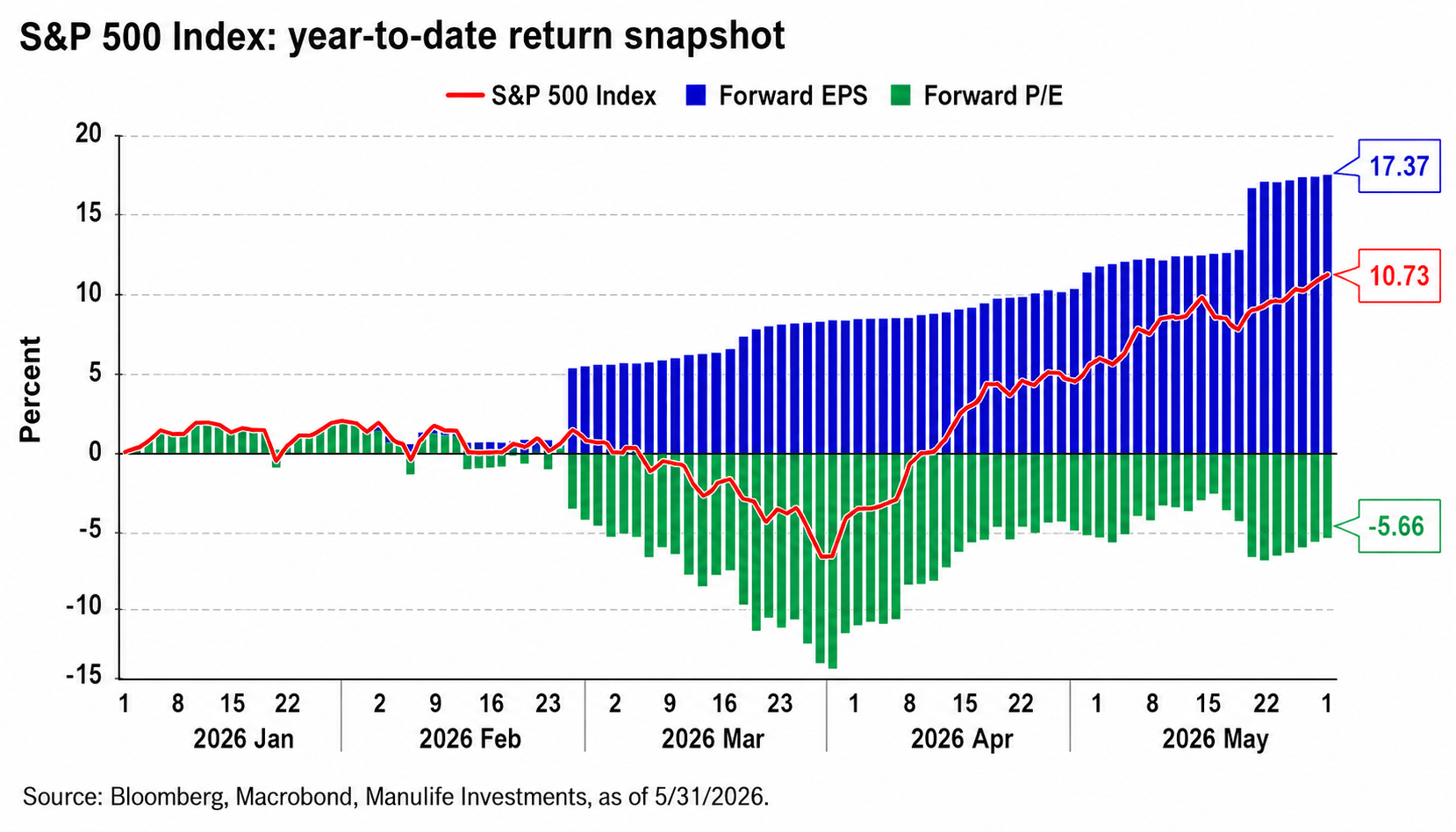

The U.S. equity market looked past the headlines and reached new highs during the month, led by large‑cap technology and semiconductor stocks. Earnings growth remained robust, reinforcing confidence that many leading firms can continue to grow their profits even as economic conditions normalize.

However, U.S. market leadership remains narrow, with a relatively small group of companies accounting for a disproportionate share of S&P 500 Index returns. Valuation levels increased from their March bottom, suggesting that the market is more sensitive to surprises—positive or negative.

Energy prices spiked early in the month amid heightened Middle East tensions, before easing toward the month‑end. While inflation has moderated from its recent peaks, episodes like the Middle East conflict highlight how quickly geopolitical events can reignite inflation risks and concerns.

Major global central banks continue to signal caution on monetary policy, reinforcing expectations that interest rates may remain higher for longer than many investors previously anticipated. The U.S. Federal Reserve (Fed), for example, appears to be shifting toward a less dovish policy stance in recent months.

Equity markets were additionally buoyed by the increased likelihood of a U.S.-Iran deal to materially reduce geopolitical risk in the region. Discussions are ongoing, with a lasting deal far from certain, but any positivity surrounding the conflict tends to relieve pressure on oil prices and reduce the perceived risk of enduring inflationary pressures.

Bottom Line

The month of May echoed a familiar theme: Markets can move higher even amid uncertainty, but returns are becoming more selective. Staying invested, diversified, and focused on long‑term goals remains the most effective portfolio strategy as markets navigate a world shaped by potentially higher rates and persistent geopolitical complexity.

Canada Recession?

Canada’s first-quarter GDP release—a large miss accompanied by downward revisions—is likely to push the Bank of Canada (BoC) back toward a more dovish policy stance. GDP shrank 0.1% quarter-over-quarter, instead of the modest 1.5% growth expected. The fourth-quarter 2025 figure was also revised down from -0.6% to -1.0%.

This was the third GDP decline in the past five quarters. Household consumption and inventories made positive contributions to growth, as anticipated, but investment failed to rebound. Ongoing weakness in the housing market and lower spending on engineering structures explain the disappointment. Non-residential and machinery and equipment investment grew only 0.5%, in line with Canadian businesses’ very slow adaptation to U.S. tariffs.

Net trade made a large negative contribution to growth. Imports rose, but mainly due to stronger demand for gold. Meanwhile, U.S. tariffs continued to hurt exports of motor vehicles, partially offset by higher shipments of crude oil and natural gas.

The odds of a BoC rate increase by the end of 2026 have dropped, with only one full hike currently priced in at the time of writing, versus four just two weeks ago. And rightly so: Facing a potential rise in core inflation due to the Iran conflict, the BoC signaled in April its willingness to hike if necessary to contain inflation spillovers.

While the Strait of Hormuz is still significantly disrupted, Canada’s starting point in terms of both growth and inflation now looks much weaker, limiting businesses’ ability to pass on higher input prices to consumers and, at the same time, giving the BoC ample room to consider if inflation is becoming a problem again.

In the current context, we continue to forecast no change in the policy rate this year.

While two consecutive quarters of negative GDP growth are considered a technical recession, we believe Canada is still far away from recession territory. The first quarter saw only a slight decline and seems more reflective of today’s uncertain environment around trade and geopolitical risks, rather than an entrenched weakening of the economy.

Playoffs and Portfolios

By the time you read this, Rob’s beloved Montreal Canadiens have been eliminated from the 2026 NHL Playoffs. Like corporate earnings season, the Canadiens exceeded expectations and drove up expectations going forward.

The NHL Playoffs once again highlight the difference between the regular season and the playoffs. While the regular season often rewards teams with higher scorers, the playoffs are often a reminder that defence matters. Take the Colorado Avalanche as a perfect example: They were the highest-scoring NHL team this season, only to be swept in the Conference Finals by one of the regular season’s worst offensive teams.

Legendary U.S. college football coach Paul "Bear" Bryant is known for coining many famous quotes. One that's stuck with me because it applies to investing, ever more so in today’s environment, is that “offence sells tickets, but defence wins championships."

Similar to building resilient long-term portfolios, the most successful sports teams are able to effectively combine offence and defence to win championships.

Looking Forward: the Middle East and CUSMA Review

As we look to June and beyond, with earnings seasons behind us, markets will be focused once again on the news headlines.

There will likely be renewed sensitivity to events in the Middle East and the wait for a steadier, more durable resolution to the conflict, which remains a big swing factor for oil prices and inflation expectations. While markets have largely absorbed recent developments, further disruptions or tensions could quickly weigh on investor sentiment, while a positive outcome could support continued upward market momentum.

There will also be trade-related macro headlines toward the end of June as Canada, the United States, and Mexico prepare for the six-year review of the CUSMA (Canada-US-Mexico Agreement), also known as USMCA (US-Canada-Mexico Agreement), but we view this as probably being more of just a checkpoint than a turning point for North American trade.

CUSMA includes a scheduled six‑year review designed to assess how the agreement is functioning.

The United States retains the legal ability to withdraw with notice, so expect tough language, targeted disputes, and possibly narrow adjustments or side agreements. While headlines may suggest rising trade risks, the most likely outcome is an extension of the agreement with limited, targeted adjustments, rather than a wholesale rewrite.

The review process may introduce short‑term uncertainty for many businesses that need to make cross‑border investment decisions, particularly in autos, manufacturing, and energy. However, the deep integration of North American supply chains means that any material disruptions would be economically costly for all parties, which acts as a stabilizing force.

We expect periodic bouts of headline-driven market volatility, especially if trade rhetoric were to intensify, but history suggests that markets tend to look through the short-term “noise” provided that the core longer-term framework remains intact.

Source: Manulife Asset Management May/2026